So many people are getting interested in managing their finances. A lot had asked me what the first step is in handling their hard-earned money. And the best answer is to get financially educated.

In my pursuit to be financially free myself (hoping to retire before 50 years old), I would like to share. It is a step by step pyramid which the Chief Executive Officer of The Global Filipino Investors himself, Floi Wycoco, had advised us to follow. But first, let’s understand what being financially free means at its simplest sense.

In my pursuit to be financially free myself (hoping to retire before 50 years old), I would like to share. It is a step by step pyramid which the Chief Executive Officer of The Global Filipino Investors himself, Floi Wycoco, had advised us to follow. But first, let’s understand what being financially free means at its simplest sense.

FINANCIAL FREEDOM

The Cashcow Couple, voted as the 2016’s Best Personal Finance Blog, defined it as “the point where your assets (stocks, bonds, real estate, etc.,.) are earning enough passive income to cover your baseline expenses.” Basically it means being “free” from needing a job to pay your dues. If you do not need to work, so to speak, then you can take the label, “financially free”.

Some people say that not having a job is just a myth and it also goes with the saying, it’s not possible. Yet, it’s still worth trying. After all, the outcome is in your favour. What do you have to lose?

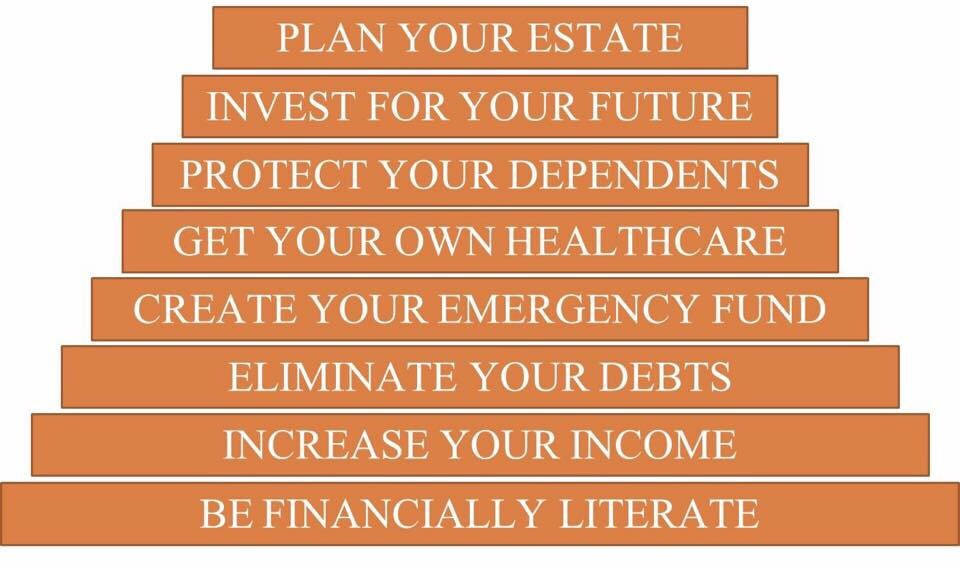

Here’s the pyramid and you gauge your ability to do goal setting.

The lowest level is the start of the journey and it is the most important. If you would think about it, it’s the best investment you could ever do for yourself. The top-level is the one you try to carry out in general and the ultimate investment once you have safety nets in accomplishing each level. It’s pretty self-explanatory as you read and assess each step.

Right now, you are actually in Step 1 that’s why this post had interested you. You are probably still in the process of thinking how you’d further increase your income flow as you go and try to figure out what else you can do beyond Step #2. Step #3: eliminating your debts, that’s when this post might come in handy.

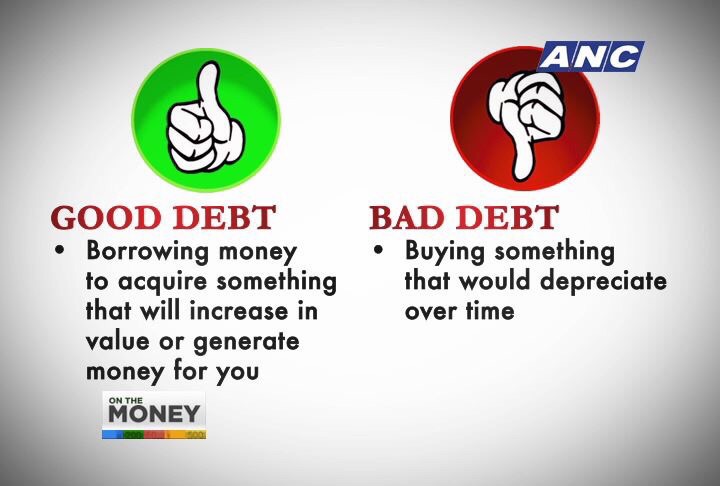

Let’s define what debt is.

DEBT

Debt is borrowing money with a promise of paying it back. Now, you might have come across what you call good debt and bad debt. Let’s see what’s the difference between the two:

Examples of good debt are usually business loans. And the best example of bad debt, is credit card debt. (Depending on the knowledge of the credit card holder, having a credit card debt may help you get a good credit score. I will feature this in my next post.)

Why is it important to know these?

Allow me to share my story.

I had an awful experience with credit card debt when I was still single. Sad to say, my credit score suffered for more than 3 years because of this. Identity theft had led me to owing my bank a sum of 60k worth of airfares that I didn’t even buy on top of my own irresponsible shopping worth 50k. After a lot of confirmation and verification, I had convinced my bank that I didn’t buy the airfare so they disregarded it but I needed to cut the card so that no further online ordering will happen.

I was bound to fly for my holiday vacation the next day but our hotel was booked using my card. So while a mix up with my credit card had happened, I had no way to secure my booking. Standard Chartered Bank was willing to change the card at my convenience provided I settle my bill of 50k first. I have to remind you, I was irresponsible. I was impulsive with my purchases that I had maxed out the card without an actual plan to pay it. Fast forward, I learned my lesson not to throw out that much money in something that didn’t actually benefit me in the end financially. I regained my credit score back, was issued of a credit card again, but because of such bad experience (yet a blessing in disguise because it made me mature in handling finances), I would know how to use it .

I remember the very mistake I made, paying only the “minimum amount” each time. As I choose to be financially literate, it dawned on me that paying the least was a mortal sin, it pays only the interest made from the unpaid bill. Then sometimes, as I pay, I use the card again and so the interest on each item purchased compounds. Right now, I can talk about it because I’ve surpassed it. So to those who are currently paying their bad debts, just keep on going. It’ll come about, trust me.

KEEPING A GOAL IN MIND

Now I am married, I have a beautiful daughter and currently raising my little family. I can tell I have become more responsible with my priorities. Spending time with my husband and daughter is much more appealing than hanging out with friends at the mall or for happy hour (though there’s a need for the latter occasionally, take it from me!), that usually don’t eat up too much of my money. Of course, expenses scaled up on a different level. But my drive to provide scaled up at the same time.

Later on, I found myself minding the finances, balancing out income with expenditures. In pursuit of staying at home most of the day, to attend to my growing toddler, I came across jobs that you could do at home. I stumbled into jobs online. The next thing I know, I stumbled into stocks, investments and trading. I can’t take much risks as much as before with my savings. So, I sought help.

I got into financial education of varied forms and got hold of the fundamentals. I guess I was giving too much energy and effort on it that eventually, the universe gave me the same energy back because. Fate made me meet people who had the same drive, which was the best part of this journey. Since we had the same goals, I had found a group that pushes me during moments of plateau, procrastination and laziness. When I am in the zone for any of those three, they encourage me to get back on my feet. And in return, I find myself encouraging them too to strive for the best financial status to continuously provide for my family satisfactorily.

I am sharing this to you all because I would like to impart the fact that (1) you could attain something wherever you put your mind into. If you work hard for a goal that you’ve set yourself with, go for it hardcore. Achievement is the result anyway. And that means, at the end of it all, you are making things happen for a better you. The most important thing is, you have to take the first step. Hence, attaining financial freedom is possible.

(2) You can avoid making a mistake like I did. Sometimes, we are too stubborn to admit that we are irresponsible, compulsive and that we need help. If you rather keep something of personal level when it comes to finances, at least, do seek a professional financial advisor who is not related to you so that you won’t hesitate to even touch ‘having debts’. In coming up with a solution for a problem, you have to acknowledge the problem first.

Let me know if you agree with the steps to financial freedom that were specified in the pyramid. I might have missed something that is worth including. Be financially free my friend.

Related posts:

- PARADIGM SHIFT – three of the most phenomenal discovery of man, (time, compounding interest and savings) that has a direct effect in our lives seen in from an empowered perspective.

- A STEP BY STEP GUIDE TO SUCCESSFUL STOCK INVESTING WITH EASY INVESTMENT PROGRAM BY COL FINANCIAL, PHILIPPINES – did you know that you could gain dividends from the stocks that you buy on top of its great ability to appreciate? Maybe investing in stocks is for you.

- HOW FINANCIALLY HEALTHY ARE YOU? – This post you just read is talking about the financial ladder to financial freedom. If you want to know about the 6 Steps to Financial Health, you might need to read this. Click on!